The Tale of Two Currencies

Why Americans see a 20% gain while Europeans see 1% disappointment

If by any chance you’ve been investing in the S&P 500 using euros, you’re probably very disappointed right now. While the news shows one S&P 500 record breaking after another, your investments barely seem to move; and if you’d just saved your money in any online bank (think Trade Republic or Revolut), you probably would have made more money.

We’re all impacted by exchange rates in one way or another. We usually don’t see it because it’s hidden behind our day-to-day purchases, but sometimes it hits us hard: when planning travel, holding stocks, making direct investments, or owning properties in different countries (like many expats do).

For me (and many others), I grew up in a country where a slight change in the dollar versus the local currency would genuinely impact daily life. It has been both a risk and an opportunity. Things have become more sophisticated for me now. I live in Europe, work for an American company, invest in international assets, deal with expenses in two different countries, and travel often. Every financial decision I make involves at least two currencies, and in some months up to four.

As this has been part of many discussions lately, especially after the recent volatility between the USD and EUR, I want to explain how this all works so you don’t get tricked by the numbers and can understand when a “losing” investment is actually winning, and how to do the math before following the latest investment trend.

Same Investments, Completely Different Returns

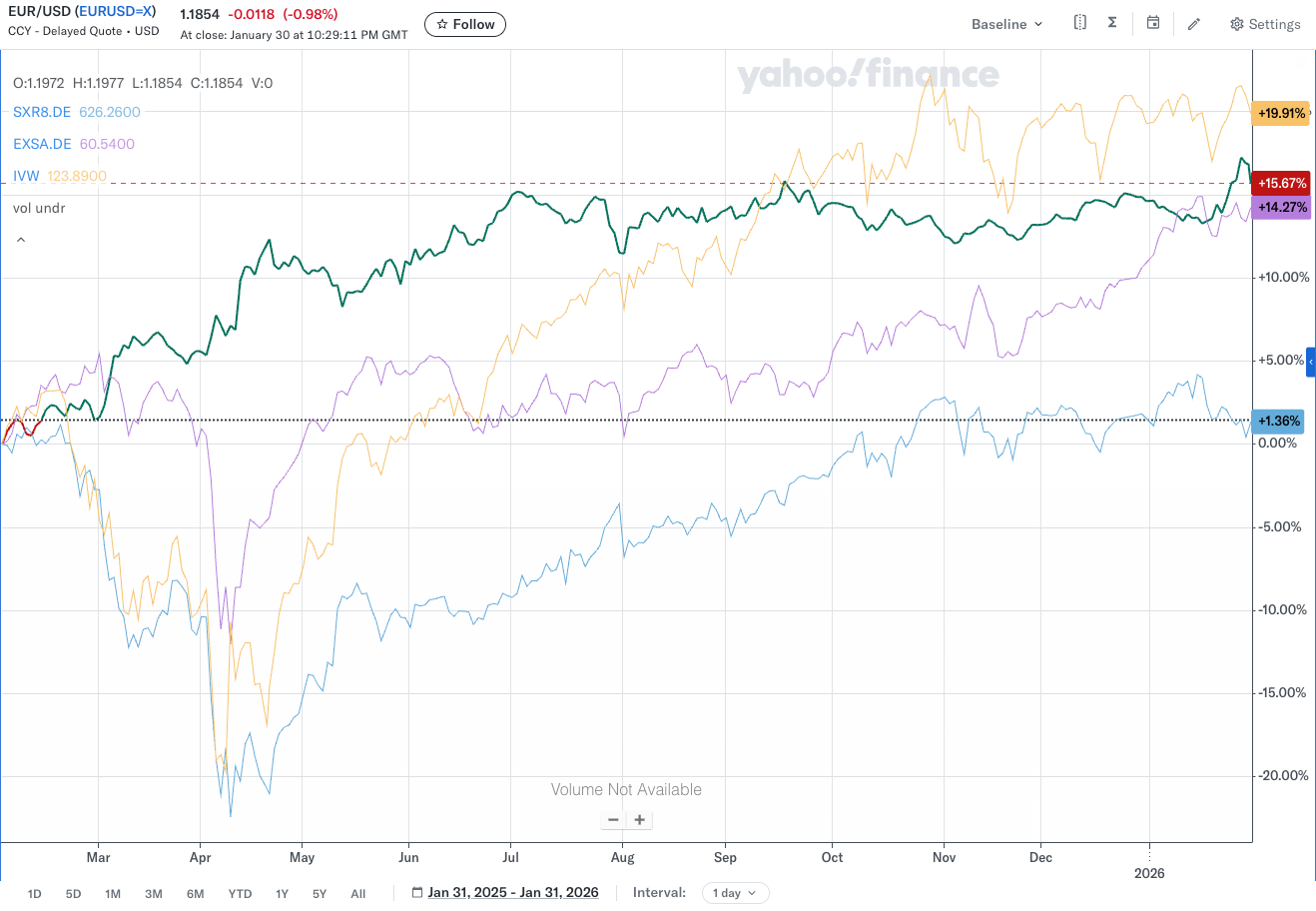

To illustrate the effect more clearly, let’s look at some real numbers.

An American investor who invested $1,000 in February 2025 in the S&P 500 iShares ETF (IVW) would have a return of 19.91% today. In other words, their $1,000 would now be worth $1,199.10.

A European investor who invested €1,000 in the S&P 500 iShares ETF (SXR8 - the European equivalent of IVW) at the same time would only see a 1.36% return. In other words, their €1,000 would be worth just €1,013.60.

The underlying S&P 500 index performed nearly identically in both ETFs—they track the same stocks. The massive difference in returns comes entirely from the EUR/USD exchange rate movement over this period.

In February 2025, the exchange rate was approximately €1 = $1.024. By the end of January 2026, it had moved to €1 = $1.1854. This ~15.7% strengthening of the euro against the dollar wiped out most of the gains for European investors.

This surprises many people, especially when following the news where every few days the S&P 500 hits a new record high. For an American investor, this is genuinely exciting news. But for a European investor, they could have invested in the “boring” European stocks index like the STOXX 600 (EXSA), which would have delivered a 14.27% return instead, without any of the AI hype.

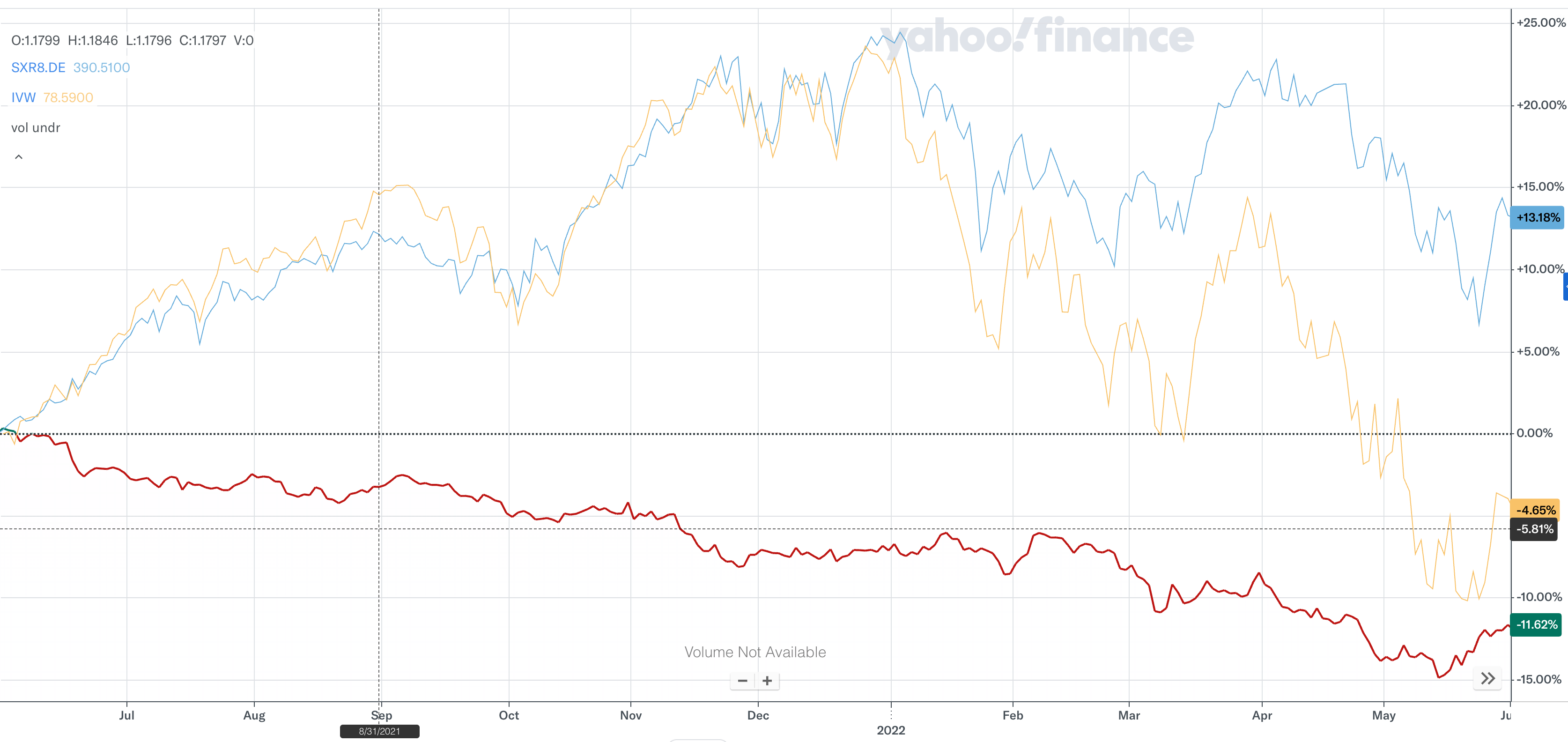

The Opposite Can Happen Too

On the complete opposite side, between June 2021 and May 2022, European investors would have been better off despite the losses in the S&P 500. During this period, the IVW ETF (the USD-based S&P 500 ETF) went down by 4.65%, but the SXR8 (the EUR-based S&P 500 ETF) increased by 13.18%. European investors would have gained money at the same time American investors lost money—of course, relative to their currency. This was mainly due to an 11.62% decline in the euro during the same period.

So why does this happen?

There’s no simple answer. Exchange rates move based on a complex mix of factors: from central bank policies to investor perception to outright speculation. This makes them nearly impossible to predict with certainty. Main drivers:

Interest rates are the primary factor. When a central bank raises rates, it typically strengthens that currency by attracting foreign investment seeking better returns. The recent EUR/USD swing partly reflects the European Central Bank’s decisions relative to the Federal Reserve’s stance.

Economic performance matters, but not always in obvious ways. Strong growth generally strengthens a currency as investors chase opportunities. But sometimes a booming economy triggers rate hikes to cool inflation, which then strengthens the currency further—creating unpredictable feedback loops.

Geopolitics and global events create ripple effects. An oil price spike in the Middle East impacts the dollar, which affects the euro. Markets often move more on perception and expectations than hard data—which is why even sophisticated quantitative models struggle to predict currency movements reliably.

This interconnectedness is exactly why currencies remain one of the hardest assets to predict, even for professionals.

And what should I do?

It’s very hard to predict exchange rate movements. I thought I had done my homework in 2025, and I was convinced the USD wouldn’t go any lower and doubled down on that assumption. It went lower—much lower than most professionals predicted.

The opposite can also happen, which is why I’ve learned to think differently and manage risks, especially around currency exposure.

For Short-Term Savings: Match Currency to Spending

The best approach for short-term savings is to hold reserves in the currency you’ll actually spend. If you need to pay something in USD a year from now, it’s better to convert and save in USD now rather than wait until the last minute and risk unfavorable rates. This is particularly common for expats buying property in their home country or planning major international trips.

You can also use Cost Averaging (CA)—converting a percentage monthly instead of all at once. This smooths out fluctuations, and you won’t feel as bad if rates move against you on any single conversion.

You should also be careful about tempting savings accounts. For example, in Europe, Revolut offers savings in USD (up to 4.18%), EUR (up to 2.02%), and GBP (up to 4.05%). The USD rate is almost double the EUR rate—but is it worth it? Looking at 2025’s exchange rate movements, keeping your euros would have been better than converting to USD despite the higher interest rate.

For Long-Term Investments: It’s More Complicated

Before we discuss long-term strategies, let’s align on some concepts. First, being too risk-averse by definition reduces your gains. I’m sure you’ve heard “no risk, no gain.” Second, you cannot avoid being impacted by currency fluctuations. The world is interconnected, and unless you live under a rock or in a cave (and I doubt you do if you’re reading this), you will be affected one way or another by other countries’ currency changes.

One option to reduce risk is hedging. Hedging, in investment, is a strategy to protect against currency risk. When you buy a currency-hedged ETF, the fund uses financial instruments (like currency futures) to offset exchange rate movements, so your returns reflect only the underlying asset performance—not currency fluctuations. Essentially, you get the stock performance as if you had invested directly in USD, but receive your returns in EUR. Sounds cool, right? Well, there are definitely some hidden issues.

Before we jump into hedging issues, let’s look at the numbers. In 2025, the S&P 500 EUR-hedged ETF (IBCF) achieved 13.4%, the USD-based version achieved 19.91%, and the unhedged EUR version achieved only 1.36%.

Have you noticed something? First, hedging costs eat into returns. Hedged ETFs charge higher fees that drain your returns over time. Also, you miss currency gains. Hedging protects you when your home currency strengthens, but it also prevents you from benefiting when it weakens.

Another consideration: currency fluctuations usually balance out over the long term. Instead of paying consistent fees every year, time will smooth things out anyway—as long as you stay invested long-term (10 to 20 years).

I know this doesn’t provide a simple answer, but that’s why many experts propose investing in diversified ETFs that aren’t solely US, EU, or Asia-focused. VWCE ETF, for example, achieved 7.35% last year and covers a multitude of stocks and countries. Yes, it will be affected by currency changes and economic turbulence, but not as severely as country-specific ETFs or even currency-hedged ones. It’s safer in the long term compared to doubling down on a specific country or industry.

The Bottom Line

Currency movements are part of investing—there’s no avoiding them. The question isn’t whether you’ll be exposed to exchange rate risk, but how you’ll manage it. Here’s what I’ve learned from getting this wrong (and occasionally right):

For money you’ll need soon, keep it in the currency you’ll actually spend. Don’t chase higher interest rates in foreign currencies unless you’re genuinely comfortable with the exchange rate risk.

For long-term investments, diversification across geographies is your best defense. Instead of trying to time currencies or paying ongoing hedging fees, spread your bets. A globally diversified ETF like VWCE won’t protect you from all currency swings, but it won’t leave you entirely dependent on any single exchange rate either.

Most importantly: Don't let exchange rates paralyze you, and don't let exciting news from other countries rush you into bad decisions. Do the math in your own currency before getting swept up in the hype. Sometimes the boring local option is actually the better investment.

A final note: This isn't investment advice—just my perspective based on experience. All the numbers come from Yahoo Finance, and while I've done my best to get them right, I can't guarantee perfect accuracy. Do your own research and talk to a professional before making any investment decisions.